Family Budget App: How to Manage Money Together Without the Arguments

Money is the number one source of stress in relationships. The right system turns it into a source of alignment.

A 2025 survey by the American Institute of CPAs found that finances are the leading cause of stress in American households, ahead of work, health, and family relationships. Seventy-three percent of couples report tension over money at least once a month. Among families with children, that number rises to 81% According to T. Rowe Price Parents, Kids & Money Survey, this aligns with broader consumer-finance trends.

The tension rarely comes from not having enough money. It comes from misalignment: different priorities, different spending habits, different comfort levels with risk, and insufficient visibility into how shared money is being used. A family budget app does not solve all of these issues, but it solves the visibility problem, and visibility turns out to be the foundation for resolving everything else.

Why Shared Spreadsheets Fail for Families

Many families start with a shared Google Sheet or Excel file. The logic seems sound: everything is visible, both partners can edit it, and it is free. In practice, shared spreadsheets fail for three predictable reasons.

Manual entry creates an uneven burden. One partner inevitably becomes the "budget person" who enters most of the transactions. The other partner contributes sporadically or not at all. This creates resentment on both sides: the tracker feels burdened, and the non-tracker feels nagged.

Retrospective tracking does not prevent problems. By the time someone enters last week's transactions into the spreadsheet, the money is already spent. There is no real-time awareness of how close a category is to its limit, which means overspending is discovered after the fact, at which point it triggers an argument rather than a course correction.

No accountability without context. When one partner sees that the other spent $200 at a store, the spreadsheet provides no context. Was it a household need, a personal purchase, or a gift? Without context, assumptions fill the gap, and assumptions in financial matters trend negative.

What a Good Family Budget App Provides

Real-Time Shared Visibility

Both partners (and potentially older children) can see category budgets, current spending, and remaining balances at any time. When you can check your phone and see that the family has $180 left in the dining budget this month, the decision about whether to order takeout becomes objective rather than contentious. "Can we afford this?" has a clear, shared answer.

Individual Autonomy Within Shared Boundaries

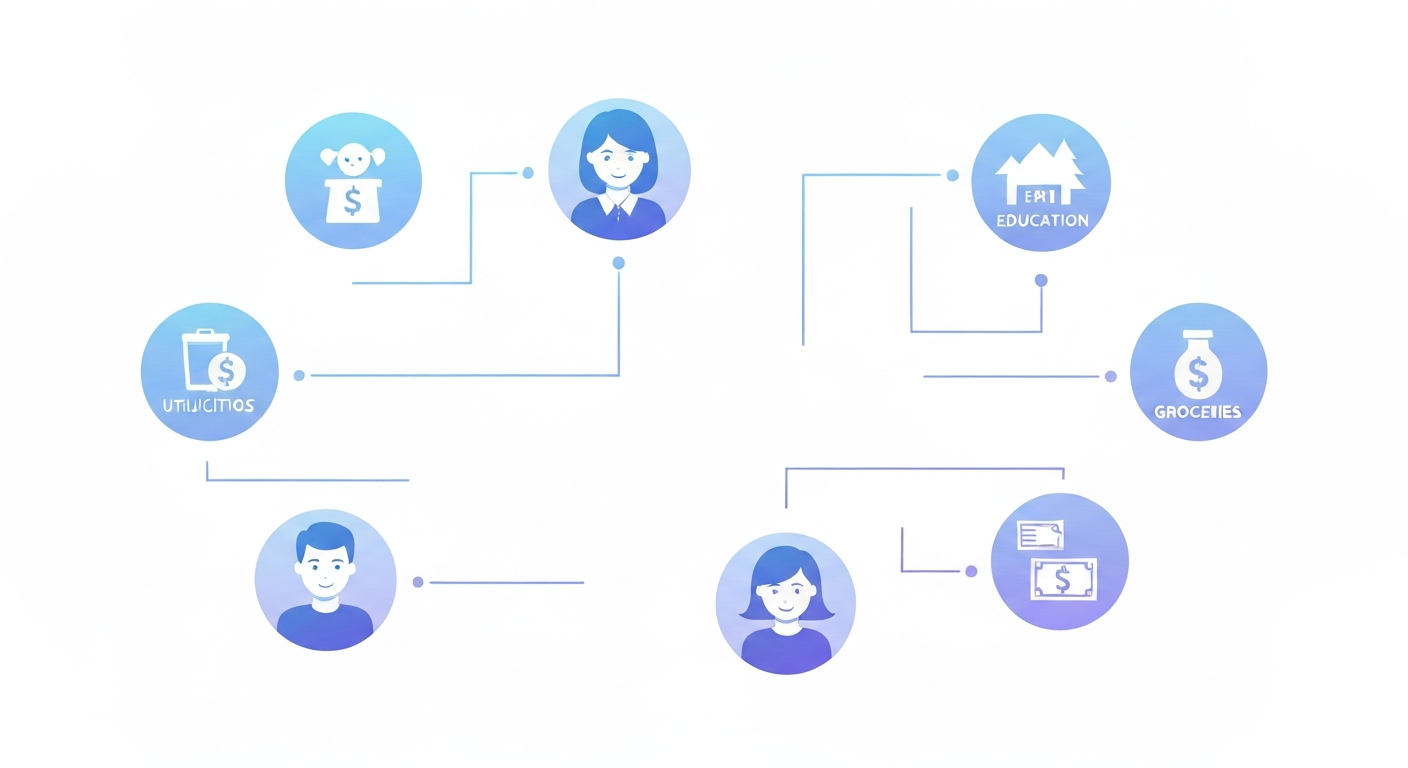

The most common failure mode in family budgeting is trying to track every dollar both partners spend. This feels controlling and creates friction over small purchases. A better approach: shared categories for joint expenses (housing, groceries, utilities, children) with clear limits, plus individual "personal spending" categories for each partner with no questions asked.

This mirrors how healthy relationships handle other shared resources. You do not need to justify every personal decision, but shared decisions require transparency and agreement. A family budget app that supports this structure, as kNexo does with its family finance features, reduces arguments because it removes the gray area about what requires discussion and what does not.

Goal Alignment Tools

Disagreements about spending often mask disagreements about priorities. One partner wants to save aggressively for a house down payment. The other wants to enjoy life now and save more gradually. Neither is wrong. They just have not aligned on shared goals.

A family budget app with goal-setting features makes these conversations concrete. Instead of arguing about abstract values ("you spend too much" / "you are too cheap"), you discuss specific targets: "If we want $40,000 for a down payment in two years, we need to save $1,667 per month. Here is what that means for our other categories."

How to Start Family Budgeting Without Causing a Fight

Step 1: Start with Observation, Not Restriction

Do not begin by cutting spending. Begin by tracking it for one full month without any limits. The goal is to establish a shared factual baseline. "This is what we currently spend" is a neutral statement. "You need to spend less on X" is an accusation. Start with the neutral statement.

Step 2: Identify Shared Non-Negotiables

After a month of tracking, sit down together and identify three things: expenses that cannot change (mortgage, insurance, minimum debt payments), savings goals you both agree on (emergency fund, retirement, specific targets), and spending areas where you are both comfortable reducing. Start with agreement, not conflict.

Step 3: Set Personal Spending Amounts

Each partner gets a monthly amount to spend however they want, no questions asked. The amount should be equal (or proportional to income in unequal-income households). This eliminates 80% of the "why did you buy that?" conversations while maintaining shared accountability for household spending.

Step 4: Weekly Check-Ins (15 Minutes Max)

Review spending versus budget for shared categories once per week. Fifteen minutes, no longer. Keep it factual, not emotional. "We are $50 over in groceries this week. Should we adjust meal plans for next week, or shift money from entertainment?" Brief, collaborative, solution-oriented.

Step 5: Celebrate Wins Together

When you hit a savings milestone, acknowledge it together. When you come in under budget for a month, that is a shared achievement. Gamified budgeting apps make this automatic with shared progress tracking and achievements. The psychological reinforcement of celebrating financial wins together strengthens both the habit and the relationship.

Teaching Kids About Money Through Family Budgeting

One of the underrated benefits of a family budget app is financial education for children. When age-appropriate, giving older children visibility into household finances (or a simplified version) teaches them concepts that schools do not cover: trade-offs, priorities, delayed gratification, and the relationship between income and spending.

Some families give teenagers their own budget category within the app, allowing them to manage a monthly allocation for their personal expenses. The mistakes they make with $50 per month at age 15 are far less expensive than the mistakes they would make with their first paycheck at 22 with zero financial experience.

What to Look for in a Family Budget App

- Multi-user access with role control. Both partners should have full access to shared categories. Personal categories should be private unless voluntarily shared.

- Real-time sync. If one partner logs a grocery purchase, the other should see the updated budget within seconds, not after a manual sync.

- Shared and individual goals. The app should support both joint goals (vacation fund, emergency savings) and individual goals (personal savings, hobby budgets).

- Low-friction expense logging. The easier it is to log expenses, the more consistently both partners will do it. AI-powered categorization and messaging-based input (like WhatsApp integration) reduce friction to near zero.

- Family-friendly gamification. Shared savings challenges and achievements make budgeting a collaborative activity rather than a chore administered by one partner.

Frequently Asked Questions

How much personal spending money should each partner get?

A common guideline is 5-10% of household take-home pay per person. So if your household brings home $6,000 per month after taxes, each partner might get $300-600 for personal spending. The specific amount matters less than both partners agreeing it is fair and sticking to it.

Should couples combine all finances or keep some separate?

Research from the University of Wisconsin found that couples who use a "hybrid" approach (shared accounts for joint expenses, individual accounts for personal spending) report the highest financial satisfaction. Full combination can feel controlling, while fully separate finances create blind spots. The hybrid model balances transparency with autonomy.

What if one partner refuses to budget?

Start small. Instead of asking them to track every expense, propose a single shared goal (like a vacation fund) with automatic contributions. Once they see progress toward something they care about, the resistance to broader budgeting often decreases. Forcing comprehensive tracking on an unwilling partner almost always backfires.

How do you budget with significantly different incomes?

Two approaches work well. Proportional contribution: each partner contributes the same percentage of their income to shared expenses (if one earns 60% of household income, they cover 60% of shared costs). Or equal contribution with proportional personal spending: split shared expenses 50/50 and allocate remaining income to personal categories. Choose the model that feels fair to both partners.

Ready to manage money as a family?

Join the kNexo waitlist for early access to family-friendly AI-powered budgeting.

Create free account