Family Financial Goals Planner: Set & Track Goals Together

Most families have shared dreams — a vacation, a bigger home, college funds — but no shared system for reaching them. Here is how to build a family financial goals planner that everyone actually uses.

A Federal Reserve survey found that 44% of American adults could not cover an unexpected $400 expense without borrowing or selling something. For families — where one emergency can cascade into missed rent, late tuition payments, and credit card debt — this statistic is especially alarming. A family financial goals planner is not a luxury; it is a safety net. But most families skip it because traditional approaches (spreadsheets, awkward kitchen-table meetings, separate banking apps that do not talk to each other) create more friction than clarity. The good news: modern tools make shared goal tracking as simple as sending a WhatsApp message. Our family budget app guide covers the broader landscape, but this article focuses specifically on goal planning — setting targets, tracking progress, and keeping every family member aligned.

Why Family Financial Goals Fail

Most families start the year with goals — "save $5,000 for vacation" — and abandon them by March. Three patterns explain why:

- Invisible progress: If the savings sit in a general account, nobody sees whether they are on track. A goal without visible progress feels abstract.

- Unequal commitment: One partner saves aggressively while the other spends normally. Without shared visibility, resentment builds quietly.

- All-or-nothing targets: "Save $5,000" feels overwhelming. "Save $417 this month" is manageable. Breaking annual goals into monthly or weekly milestones is the single most effective change families can make.

A proper family financial goals planner solves all three: progress is visible, contributions are tracked per member, and large goals are broken into digestible chunks. The approach mirrors what individual goal-setting research recommends, scaled to multiple people.

How to Set Family Financial Goals

The goal-setting process works best when every contributing family member has input. Here is a framework used by financial planners, adapted for self-service:

Step 1: The Family Finance Meeting

Schedule 60 minutes — once. Not monthly, not weekly, just once to establish the framework. Each family member (adults and teens old enough to contribute) answers:

- What is one financial goal you want the family to achieve in the next 12 months?

- What is one goal for the next 3-5 years?

- What is a "dream goal" with no timeline?

Combine, discuss, and select 2-3 goals maximum. More than three dilutes focus and makes tracking burdensome. The CFPB recommends including children in age-appropriate financial discussions as early as possible.

Step 2: Define SMART Goals

Convert vague wishes into specific, measurable, achievable, relevant, time-bound goals:

- Vague: "Save for vacation." SMART: "Save $4,000 for a Florida trip by December 15, 2026, contributing $500/month from the joint account."

- Vague: "Build an emergency fund." SMART: "Reach $10,000 in emergency savings by June 2027, starting from $2,400 with $500/month automatic transfers."

- Vague: "Save for college." SMART: "Contribute $300/month to 529 plans through 2032, targeting $25,000 per child."

Each goal needs an owner (who is responsible for the monthly contribution), a tracking mechanism, and a monthly check-in date. For emergency fund specifics, our emergency fund guide walks through the math.

Step 3: Choose a Tracking Tool

The tool matters less than the habit, but the right tool reduces friction. Options ranked by family-friendliness:

- kNexo's Family ($29.90/month billed annually): Supports up to 6 family members, shared goals visible to all, individual privacy on personal spending, AI categorization, WhatsApp logging. The gamification features — missions and streaks — keep teens and kids engaged alongside adults.

- Honeydue (free): Designed for couples. Shared bills, coordinated budgets, and a chat feature. Good for two-person households but lacks kid/teen profiles.

- Goodbudget ($10/month paid tier): Shared envelope budgets accessible from multiple devices. Manual entry, no AI. Works well for families who prefer hands-on tracking.

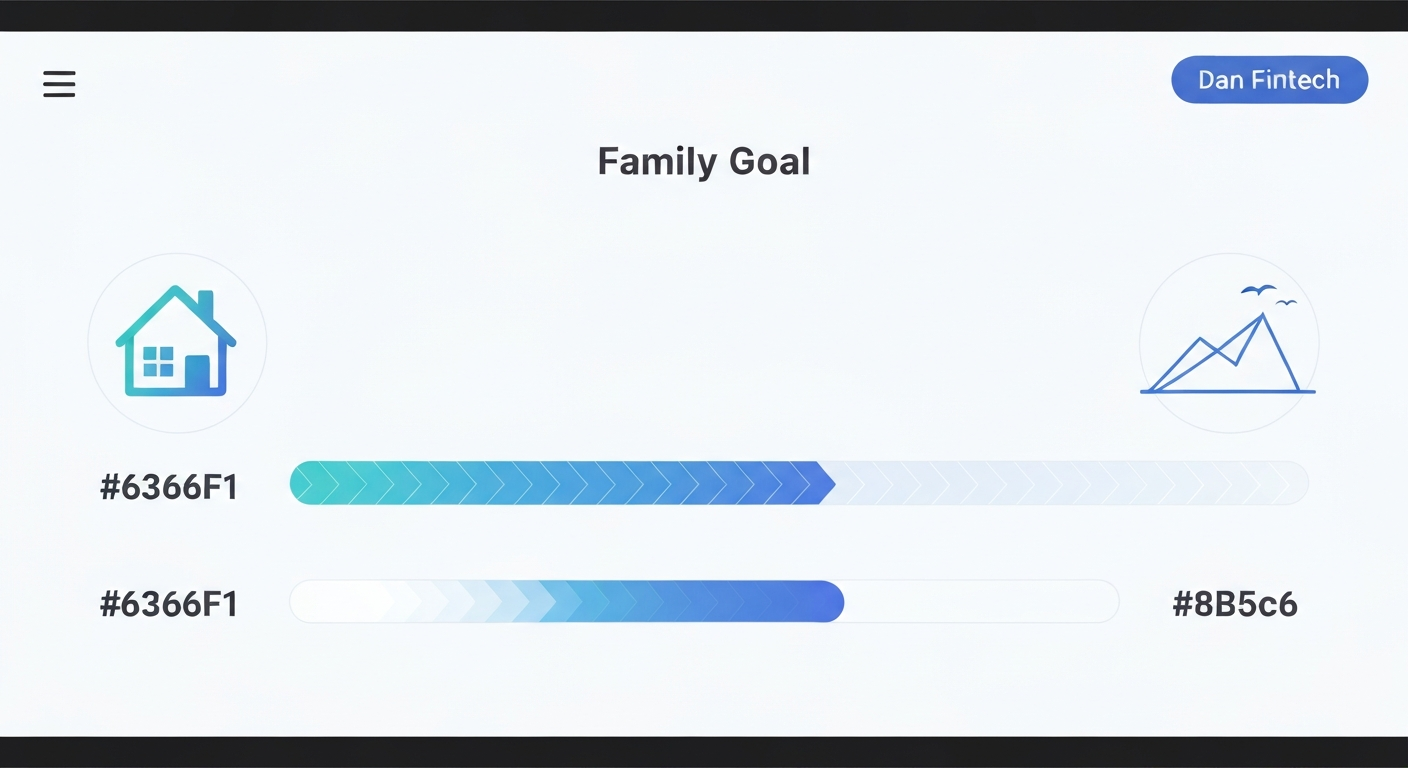

The family that sees their vacation fund grow from $0 to $2,000 together experiences a shared win that no spreadsheet can replicate. Visible progress is the glue that holds family financial goals together.

The Monthly Check-In Framework

After the initial setup, the ongoing work is a 15-minute monthly check-in. Here is the agenda:

- Progress review (5 min): Are we on track for each goal? If not, what slipped?

- Adjustments (5 min): Does any goal need to be adjusted? Life changes — new expenses, income shifts — require goal flexibility.

- Celebration (5 min): What went well? Did we hit a milestone? Even small wins ("We crossed $1,000 in the vacation fund!") deserve acknowledgment.

Keep it short. Long financial meetings create dread, which leads to avoidance, which leads to missed goals. If you use kNexo, the app handles progress tracking automatically — the check-in becomes a review session, not a data-entry session.

Goal Categories for Every Family Stage

Not every family needs the same goals. Here are the most common categories by life stage:

Young Families (Kids Under 10)

- Emergency fund: Target 3-6 months of expenses. The NerdWallet recommendation is 6 months, but 3 months is a realistic starting point.

- 529 college fund: Even $100/month per child grows significantly over 18 years.

- Family vacation fund: A shared, visible, rewarding goal that keeps everyone motivated.

Families With Teens

- Car fund: Teen contributes 50%, parents match — teaches goal partnership.

- Home improvement: Practical family goals teens can see and appreciate.

- Teen savings goals: Individual goals tracked within the family app. See our teen budgeting guide for age-appropriate approaches.

Dual-Income Households

- House down payment: Target 20% to avoid PMI. At $400,000 home value, that is $80,000 — a multi-year goal that needs visible tracking.

- Early retirement fund: Beyond 401(k) contributions, additional savings in taxable accounts.

- Debt elimination: Treat debt payoff as a shared goal with celebrated milestones.

The 70-10-10-10 Rule for Families

The 70-10-10-10 budget rule simplifies family allocation:

- 70% — Living expenses (housing, food, transport, utilities, insurance)

- 10% — Short-term savings (emergency fund, vacation, goals)

- 10% — Long-term investments (retirement, 529s, taxable accounts)

- 10% — Giving or additional debt repayment

For a family earning $8,000/month after taxes, that is $5,600 for expenses, $800 for savings goals, $800 for investments, and $800 for giving/debt. kNexo's AI can automatically categorize transactions into these buckets, showing in real time whether the family is hitting the 70-10-10-10 targets.

Keeping Everyone Engaged

The biggest risk to a family financial goals planner is one member disengaging. Prevention strategies:

- Visual progress: Use an app with progress bars or percentage-complete indicators. Seeing "67% to vacation fund" is more motivating than a spreadsheet number.

- Individual wins: Alongside shared goals, each member should have at least one personal goal. Teens saving for headphones, adults saving for a hobby purchase — personal wins reinforce the system.

- Low-friction updates: kNexo's WhatsApp integration means contributions update automatically when expenses are logged — no manual data entry required from any family member.

- Gamification for kids: kNexo missions turn saving into a game. A child earning a "$50 saved" badge feels personal accomplishment, not parental obligation.

The Bottom Line

A family financial goals planner works when it does three things: makes progress visible, assigns accountability to individuals within the family, and keeps check-ins short enough that nobody dreads them. kNexo's Family handles all three with shared goals, per-member tracking, WhatsApp convenience, and gamification that keeps kids and teens engaged alongside adults. Start with 2-3 goals, break each into monthly targets, and schedule a 15-minute monthly review. The families who plan together are the families who reach their goals — and the tools have never made it easier to start.

Frequently Asked Questions

What is the best app to create a household budget?

kNexo's Family supports up to 6 family members with shared goals, individual privacy controls, and AI tracking via WhatsApp. Goodbudget and Honeydue are alternatives for couples.

What is the 70-10-10-10 budget rule?

It allocates income into four buckets: 70% living expenses, 10% savings, 10% investments, and 10% giving or debt repayment. It is simpler than zero-based budgeting and works well for families who want clear categories.

How do families set financial goals together?

Hold a one-time 60-minute family meeting to identify 2-3 shared goals. Define targets and timelines. Use a shared tool like kNexo for tracking. Schedule 15-minute monthly check-ins to review progress and adjust.

Should couples combine finances or keep them separate?

Research suggests partially merging finances produces the highest relationship satisfaction. A shared account for joint expenses plus individual accounts for personal spending works for most families. kNexo's Family supports this with individual privacy controls.

Ready to take control of your finances?

kNexo turns AI into your money copilot — right inside WhatsApp. Free forever, no credit card.

Create free account